ISC Economics Previous Year Question Paper 2010 Solved for Class 12

Maximum Marks: 80

Time allowed: 3 hours

- Candidates are allowed additional 15 minutes for only reading the paper.

- They must NOT start writing during this time.

- Answer Question 1 (Compulsory) from Part I and five questions from Part II.

- The intended marks for questions or parts of questions are given in brackets [ ].

Part – I (20 Marks)

Answer all questions.

Question 1.

Answer briefly each of the questions (i) to (xv): [15 × 2]

(i) What is micro economics? Give an example.

(ii) How is exante demand different from expost demand?

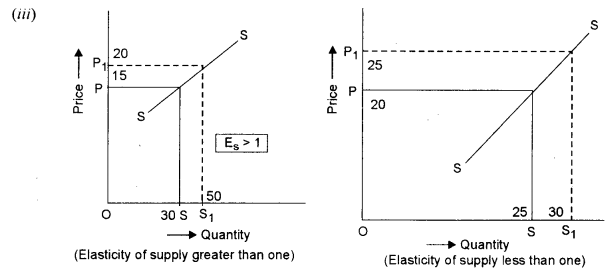

(iii) Draw two supply curves, the first one showing elasticity of supply greater than one and the second one showing elasticity of supply less than one.

(iv) Define marginal revenue. How can we get marginal revenue from total revenue?

(v) Explain two advantages of international trade.

(vi) What is meant by actual earning of a factor?

(vii) How is Net National Product at factor cost obtained from Net National Product at market price?

(viii) Distinguish between productive debt and unproductive debt citing an example of each.

(ix) Mention two similarities between perfect competition and monopolistic competition.

(x) Define Balance of Trade.

(xi) Differentiate between consumer goods and producer goods. Give one example of each.

(xii) Identify whether the costs stated below are implicit costs or explicit costs. Justify your answer for each:

(a) Rent for self owned land.

(b) Payment made for advertising.

(xiii) What is meant by a balanced budget?

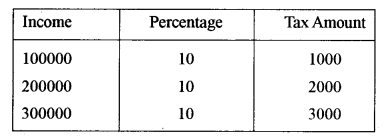

(xiv) Define proportional tax and show it graphically.

(xv) When can the equilibrium price remain unaffected by a change in demand? Show with the help of a diagram.

Answer:

(i) Microeconomics, the study of the economic behaviour of small economic groups such as firms and families, is one of the largest subfields in economics. These resources will help you ace your test, get a good mark on your microeconomics term paper, and help you understand how economic decisions are made.

(ii) Demand may be viewed ex-ante or ex-post: Ex-ante demand is the intended demand and ex-post demand is what is already purchased. The former denotes potential demand, while the latter refers to the actual magnitude purchased.

(iv) Marginal revenue is the additional revenue added by an additional unit of output, or in terms of a formula:

Marginal Revenue = (Change in total revenue) divided by (Change in sales)

(v) Advantages:

- International trade brings in different varieties of a particular product from different destinations.

- Promotes efficiency in production as countries will try to adopt better methods of production to keep costs down in order to remain competitive.

- Brings foreign exchange to the exporting countries. It makes the foreign currency reserves healthy.

(vi) Actual earnings of a factor tell you how healthy that factor is and if it may pay dividends or grow through capital appreciation (higher price).

(vii) Net national product at factor cost can be obtained from Net National Product at market price in the following manner.

Net National Product at Factor Cost = Net National Product at Market Price – Indirect Taxes + Subsidies.

Or

Net National Product at Factor Cost = Net National Product at Market Price – Net Indirect Taxes

(viii) Productive debt is used to purchase a productive asset: i.e.. one that will produce a profit while serv icing the debt. Debts used for the purchase of a rental property, equipment for a business, or perhaps dividend-paying stocks can be considered “productive” if they earn a profit. Unproductive debt is the debt used to finance activities that did not increase productivity.

Unproductive debt is that debt which is incurred to cover any budgetary deficits or for such purposes as do not yield any income to the government in times of war for example. The interest and sinking fund, if any, on this type of debt must be obtained from some other source of public income, generally from taxation and, since there is no corresponding asset created, there is no rule regarding the period of repayment.

(ix) Similarities between perfect and monopolistic competition.

- Many numbers of sellers and buyers in both type of markets.

- Free entry and exit of the firms.

(x) Trade account of the balance of payments includes exports and imports of goods in a year. The difference between the value of exports of goods and value of imports of goods is called the balance of trade. For example, if the value of the exports of goods is Rs. 10,000 in a year and the value of imports in the same year is Rs. 6,000, then the balance of trade is (+) Rs 4,000. It is a surplus balance of trade as exports are greater than imports.

(xi) Any tangible commodity purchased by households to satisfy their wants and needs. Consumer goods may be durable or non-durable. Durable goods (e g., autos, furniture, and appliances) have a significant life span, often defined as three years or more, and consumption is spread over this span. Non-durable goods (e.g., food, clothing, and gasoline) are purchased for immediate or almost immediate consumption and have a life span ranging from minutes to three years.

Goods manufactured and used in further manufacturing, processing or resale. Producer goods either become part of the final product or lose their distinct identity in the manufacturing stream.

(xii) (a) Implicit Cost.

A cost that is represented by a lost opportunity in the use of a company’s own resources, excluding cash is an implicit cost.

(b) Explicit cost

A business expense that is easily identified and accounted for is taken under explicit costs.

(xiii) A budget in which revenues equal or exceed expenditures. A balanced budget is thought to be positive for a company, as it means that the company is not taking on any (additional) debt in order to conduct its operations; if revenues exceed expenditures, it results in a profit.

(xiv) Proportional is a tax system in which the rate of taxation (percentage) remains constant at all levels of income (regardless of how much an individual earns.).

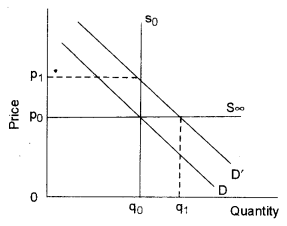

(xv) If the supply of the goods is perfectly elastic, change in demand would not affect the equilibrium price.

Part – II

(Answer Any Five Questions)

Question 2.

(a) In a straight-line demand curve touching the two axes, show the different degrees of elasticity of demand. [4]

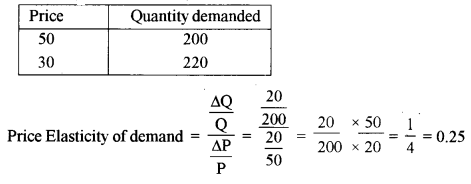

(b) The price of a commodity falls from Rs. 50 to Rs. 30, resulting in an increase in the purchase of the commodity from 200 units to 220 units. Calculate the price elasticity of demand. [4]

(c) State the Law of Demand with two assumptions. Briefly discuss two exceptions to the Law of Demand.

Answer:

(a)

Three degrees of elasticity of demand are possible when the demand curve touches two axes

- Inelastic demand

- Unit elastic demand

- Elastic demand (greater than unit)

(b)

(c) The law of demand is stated as “other things being equal, the quantity demanded increases with a fall in price and diminishes with a rise in price”. According to this law other things being equal, demand varies inversely with the price that is, at a higher price less will be demanded and at a lower price more will be demanded.

Assumptions to the Law of Demand

(i) Tastes and preferences of the consumer are the same regardless of the income group.

(ii) All consumers have a fixed income and there is no change in income over a period of time.

(iii) Thirdly, the prices of the related goods do not change and they are fixed.

The law of demand states that, if all other factors remain equal, the higher the price of a good, the fewer people will demand that good. In other words, the higher the price, the lower the quantity demanded. The amount of a good that buyers purchase at a higher price is less because as the price of a good goes up, so does the opportunity cost of buying that good. As a result, people will naturally avoid buying a product that will force them to forgo the consumption of something else they value more.

Exceptions to the Law of Demand

Giffen goods: These are those inferior goods on which the consumer spends a large part of his income and the demand for which falls with a fall in their price.

Articles of snob appeal: Goods which serve status symbol do not follow the law of demand. These are goods of conspicuous consumption. These goods give their possessor utility in the sense of their ownership. Articles like diamond are purchased by the rich irrespective of their price hike as their possession is prestigious. When their price rises the prestige value goes up.

Question 3.

(a) Discuss two differences between micro and macroeconomics. [4]

(b) With the help of diagrams, show the shift and movement on the demand curves. [4]

(c) Using the utility’ approach, discuss how a consumer attains equilibrium. [6]

Answer:

(a) Microeconomics is the study of economics from a more individual point of view (consumers and their spending habits and firms in how they make profits) and how the economy affects people in their daily lives. Macroeconomics is economics from a ‘big picture’ perspective, such as how our country’s economy affects the world as a whole, etc.

Macroeconomics deals with large-scale economic decisions. It focuses on countries or continents and large regions, and it generally has applications for government policymakers. In contrast, microeconomics focuses on small-scale economic decisions, between individuals and firms. It examines how businesses can be the most successful and why individuals make the economic decisions that they do.

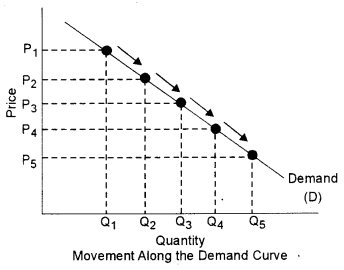

(b) Movement

A movement means a change along a curve. On the demand curve, a movement denotes a change in both price and quantity’ demanded from one point to another on the curve. The movement implies that the demand relationship remains consistent.

Therefore, a movement along the demand curve will occur when the price of the good changes and the quantity demanded changes in accordance to the original demand relationship. In other words, a movement occurs when a change in the quantity demanded is caused only by a change in price and vice versa.

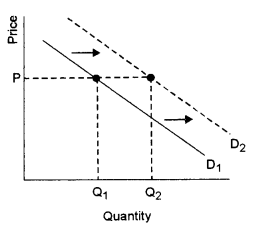

Shift

A shift in a demand or supply curve occurs when a good’s quantity’ demanded or supplied changes even though price remains the same. Shifts in the demand curve imply that the original demand relationship has changed, meaning that quantity demand is affected by a factor other than price.

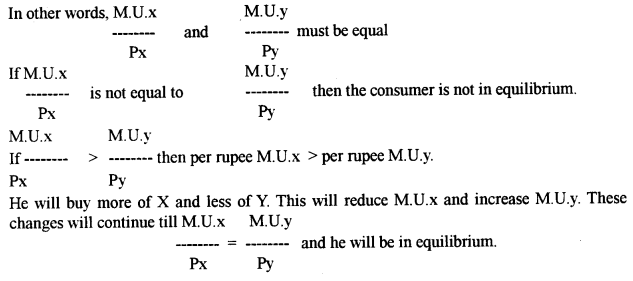

(c) A consumer will attain equilibrium if he allocates his given income on the purchase of goods X and Y in a manner that gives him maximum satisfaction.

He will get maximum satisfaction if he buys only that quantity of each good that gives him the same utility from the last rupee spent on each good.

Question 4.

(a) Distinguish between monopoly and monopolistic competition on the basis of average revenue curves and entry of firms. [4]

(b) What is meant by returns to scale? Differentiate between short-run production function and long-run production function. [4]

(c) Show how a firm in a perfectly competitive market earns normal profit in the long run. [6]

Answer:

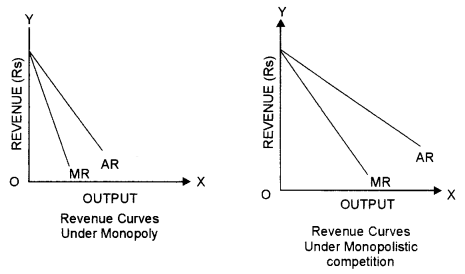

(a) The distinction between Monopoly and Monopolistic Competiton On the basis of Average Revenue:

Under monopoly, average revenue and marginal revenue curves are two separate curves.

AR curve represents the price of different units and MR curve represents the marginal revenue of different units. Both the curves are downward sloping, meaning thereby that if the monopolist intends selling more units, he will have to lower the price per units.

Under monopolistic competition also, AR and MR curves are two separate curves. The slope > downward from left to right. But both these curves are more elastic than the curves under monopoly.

On the basis of Entry of Firms:

Under monopolistic competition, there are no restrictions on the new firms to enter into and the old ones to leave the group. However, this entry and exit are not so easy in the short-period. It is possible in the long-run only. But under a monopoly, there are restrictions on the entry of new firms.

(b) The quantitative change in the output of a firm or industry resulting from a proportionate increase in all inputs. If the quantity of output rises by a greater proportion e.g. if output increases by 2.5 times in response to a doubling of all inputs-the production process are said to exhibit increasing returns to scale. Such economies of scale may occur because greater efficiency is obtained as the firm moves from small to large-scale operations.

The short-run is defined in economics as a period of time where at least one factor of production is assumed to be in fixed supply i.e., it cannot be changed. We normally assume that the quantity of capital inputs (e g., plant and machinery) is fixed and that production can be altered by suppliers through changing the demand for variable inputs such as labour, components, raw materials and energy inputs. Often the amount of land available for production is also fixed. The time periods used in textbook economics are somewhat arbitrary because they differ from industry to industry. The short-run for the electricity generation industry or the telecommunications sector varies from that appropriate for newspaper and magazine publishing and small-scale production of foodstuffs and beverages. Much depends on the time scale that permits a business to alter all of the inputs that it can bring to production.

Long-run production – returns to scale

In the long run, all factors of production are variable. How the output of a business responds to a change in factor inputs is called return to scale.

Increasing returns to scale occur when the % change in output > % change in inputs.

Decreasing returns to scale occur when the % change in output < % change in inputs.

(c) In the long run, all inputs of a firm are variable. If the demand increases or decreases, all the firms have sufficient time to adjust their production according to the market conditions. In the long run, a firm can earn only normal profits because in case of continued abnormal profits new firm will enter into the market and supply will increase to meet the demand. In case of continued losses, certain firms will reduce their products or a few may leave the industry. In this case, the supply shall be reduced and the price will come up to its normal level. When a firm is, earning a normal profit in the long run, it will express the following equation. Marginal revenue (MR) = Marginal Cost (MC) = AC = AR = Price. So MR = MC = AC = AR = Price.

All the competitive firms, in the long run, earn normal profit and there is so tendency for the new firms to enter or leave the industry; they are in equilibrium when all the firms in the industry are in the state of lull equilibrium equating price, marginal revenue, marginal cost, average total cost, to the industry itself is also in equilibrium. When the industry is also in the long equilibrium there is an optimum allocation of resources. The consumers will get the commodity at a lower price because goods are produced at normal profit in the long run.

Question 5.

(a) Show the circular flow of income in a two-sector model with leakages and injections. [4]

(b) Discuss the problem of double counting in the estimation of national income. [4]

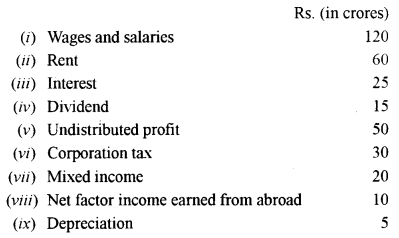

(c) Calculate national income and gross domestic product at factor cost from the following data: [6]

Answer:

(a) An Economy can be classified in various ways. One such way is purely theoretical. In this context, there are four sectors of an economy. These are households, firms, government and the rest-of-the-world. If we consider only the first three sectors, it becomes a closed economy. Inclusion of the last sector (also called the foreign sector) makes it an open economy. Considering only the first two sectors, it becomes a two-sector model;

Circular flow of income model is a model used to show the flow of income through an economy. Through showing the leakages in the economy and the injections, the different factors affecting the economic activities are apparent. Just like leakage in a fish tank, a leakage in the economy. leads to a decrease in economic activity.

And just like an injection into a fish tank where the water level rises, an injection in an economy leads to an increase in economic activity. To understand how the circular flow of income can be used to show disequilibrium in the economy you must first understand what disequilibrium is. Disequilibrium is the state where economic activity is not equal, that is where leakage > injections or when leakages < injections. whereas the state of equilibrium is when leakages = injections. Hence disequilibrium is when the savings are either greater or less than the investment.

(b) To calculate national income overall value of goods and services produced by the country is taken into account. However, this method suffers from ‘double counting. ’ Since the output of a production unit can be the input for another unit, it leads to double counting of a single variable.

Only final goods are included when measuring national income. If intermediate goods were included too, this would lead to double counting; for example, the value of the tires would be counted once when they are sold to the car manufacturer, and again when the car is sold to the consumer.

(c) GDP = Wages and Salaries + Rent Paid + Interest Paid + Dividend Paid

= 120 + 60 + 25 + 15

= 240

National Income = GDP – Depreciation + Net Factor Income + Mixed-Income + Undistributed Profits – Corporation Tax

= 240 – 5 + 10 + 20 – 30

= 225

Question 6.

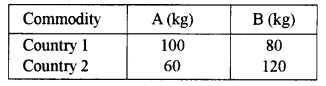

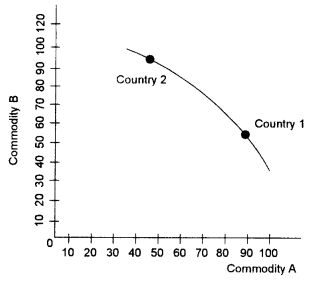

(a) The following table shows the production of two commodities A and B, manufactured by Country 1 and Country 2, using one labour each. [4]

(i) Draw the opportunity cost curves for Country 1 and Country 2.

(ii) Name the country which will specialise in commodity A. Give reasons.

(b) Mention one difference between devaluation and depreciation of currency. How can depreciation of a currency be a measure to correct disequilibrium of Balance of Payment? [4]

(c) Explain the components of the current account of the Balance of Payment. [6]

Answer:

(a) Opportunity cost is measured by the slope of the production possibilities curve. In particular, the slope of the production possibilities curve is the opportunity cost of the good measured on the horizontal axis.

Opportunity cost is measured by the slope of the production possibilities curve. In particular, the slope of the production possibilities curve is the opportunity cost of the good measured on the horizontal axis.

(i)

(ii) The country 1 will specialize in commodity A. By using specialization, a country can concentrate on the production of one thing that it can do best, rather than dividing up its resources to produce another thing.

(b) Devaluation of Currency: Currency devaluation takes place when one country’s currency is reduced in value in comparison to other currencies. After currency devaluation, more of the devalued currency is required in order to purchase the same amount of other currencies.

For a currency to be devalued means that the issuing government has mandated that the price of the currency (in foreign dollars) is lower than it was before.

Depreciation of Currency: A decline in the value of one currency relative to another currency. Depreciation occurs when, because of a change in exchange rates, a unit of one currency buys fewer units of another currency.

The deprecation of currency is made in order to promote exports and discourage imports, as when a currency is depreciated exports become cheaper because while imports become more expensive.

(c) Components of Current Account of the Balance of Payment: The current account shows the net amount a country is earning if it is in surplus, or spending if it is in deficit.

It is the sum of the balance of trade (net earnings on exports – payments for imports), factor income (earnings on foreign investments-payment made to foreign investors) and cash transfers.

Entries under Current account might include:

Trade – buying and selling of goods and services

Exports – a credit entry

Imports – a debit entry

Trade balance – the sum of Exports and Imports

Factor income – repayments and dividends from loans and investments

Factor earnings – a credit entry

Factor payments – a debit entry

Factor income balance – the sum of earnings and payments.

Question 7.

(a) Define gross profit. How is net profit different from the gross profit? [4]

(b) Explain the components of gross interest. [4]

(c) Discuss four differences between rent and quasi rent. [6]

Answer:

(a) Gross Profit: Gross profit is calculated as sales minus all costs directly related to those sales. These costs can include manufacturing expenses, raw materials, labour, selling, marketing and other expenses.

Net Profit: Net Profit is the amount of money earned after all expenses, including overhead, employee salaries, manufacturing costs, and advertising costs, have been deducted from the total revenue.

Gross Profit is showed in the debit side in the Trading Account. Net Profit is showed in the debit side in the Profit and Loss Account.

(b) Gross interest rate: This is the total interest payable before any deductions such as tax and charges.

Components of Gross Interest:

1. Net interest: Net interest is that, which is paid for the use of the services of money alone.

2. Reward for Risk: Creditor has to take the risk in lending his money. He feels sceptical about the return of money to him. This risk can be of two types

- Business Risk: This risk arises because of the uncertainties of the business. When the business of the debtor is met with failure, then despite his good intentions, he is unable to repay the debt. Thus, the creditor runs a risk in giving loans.

- Personal Risk: It refers to the economic condition, character and integrity of the debtor. When a debtor is in a position to repay his debt but he willfully refuses to do so or he becomes bankrupt, the moneylender runs a personal risk.

3. Reward for Management: Creditor has to maintain proper account books showing different transactions regarding paying of loans, receipts of interest, balance due or repayment of the principal amount, etc. He may have to engage an account clerk for this purpose. He may have to make repeated requests to the debtor for the recovery of his dues. The expenses incurred on all these items must be adequately compensated. Thus the creditor includes his reward for management of accounts in the gross interest

4. Reward for Inconvenience: Parting with money involves several inconveniences on the part of the creditor. He may not get back money when needed and he himself may have to borrow from someone else. Or he may get his money back in small instalments. The reward for inconvenience thus figures in gross interest.

(c) (i) Rent is earned by the free gifts of nature such as land. But Quasi-rent is the excess income earned by the man-made factors.

(ii) Rent is earned both in short-run and long run. While Quasi-rent occurs only in short-run because, in the long run, man-made factors have their perfectly elastic supply.

(iii) Rent is permanent earning while Quasi-rent is transitory. In other words. Quasi-rent is not a cost in a short period.

(iv) Rent is never zero. But Quasi-rent becomes zero when the price is equal to average variable costs.

(v) Rent is the difference between total earnings and total costs. But Quasi-rent is the difference between total earnings and variable costs.

Question 8.

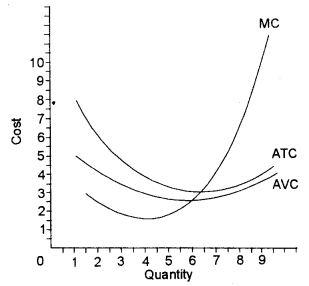

(a) Draw the average variable cost and average total cost curves. Do they intersect each other? Give one reason for your answer. [4]

(b) Discuss two exceptions to the Law of Supply. [4]

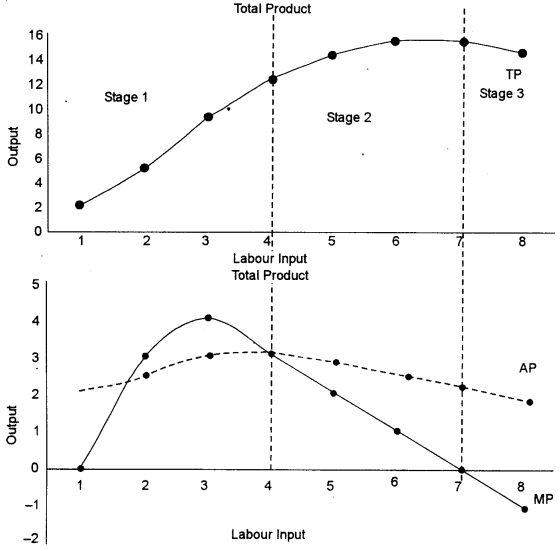

(c) ‘If more variable factors are employed with fixed factors, the total product increases at an increasing rate and finally, it falls’. Explain the three stages of the Law with the help of TP, AP and MP curves. [6]

Answer:

(a)

The Average Variable Cost Curve and Average Total Cost Curve do not intersect each other. There is a gap between the two average curves, which is the average fixed cost.

(i) Exceptions to the Law of Supply

The law of supply does not apply in the following cases:

- In the case of agricultural products whose supply is affected by natural factors.

- In the case of perishable goods like food. In the case of these goods, the seller is willing to sell more units at decaying prices.

- In the case of goods having a social distinction. The supply of goods will remain limited even if their prices are high.

(c) The AP curve and its relationship to the MP and TP curves

The average product at each point on the TP curve is given by the slope of the line joining this point to the origin. Consider the point A on the TP curve. Average product is output/labour input = AB/OB = slope of the line OA.

The three stages of production

Based on the behaviour of MP and AP, economists have classified production in three stages:

Stage I: MP > 0, AP rising. Thus, MP > AP.

Stage II: MP > 0, but AP is falling. MP < AP but TP is increasing (because of MPO).

Stage III: MP < 0, In this case, TP is falling.

Question 9.

(a) Explain two effects of deficit financing. [4]

(b) Differentiate between fiscal deficit and primary deficit. [4]

(c) Discuss four characteristics of a good tax system. [6]

Answer:

(a) Effects of deficit financing

- Deficit financing in a developing country is inflationary. It hikes the prices of the goods.

- Deficit financing for development, like depression deficit financing, provides stimulus to economic growth by financing investment, employment and output in the economy. It helps rapid capital formation for economic development.

(b) Primary deficit is one of the parts of fiscal deficit. While the fiscal deficit is the difference between total revenue and expenditure, the primary deficit can be arrived by deducting interest payment from fiscal deficit. The interest payment is the payment that a government makes on its borrowings to the creditors.

(c) Economic efficiency: The tax should not prevent the efficient allocation of resources.

Administrative simplicity: The tax should be easy and inexpensive to administer.

Flexibility: The tax system should respond easily to changes in economic conditions.

Transparency: Individuals should be able to ascertain their tax burdens so that burdens can be politically tailored to what society considers desirable.

Fairness: The tax system should be fair in its treatment of different individuals.