ISC Accounts Previous Year Question Paper 2017 Solved for Class 12

Maximum Marks: 80

Time allowed: Three hours

- Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.

- Answer Question 1 (Compulsory) from Part I and five questions from Part II, choosing two questions from Section A, two questions from Section B and one question from either Section A or Section B.

- The intended marks for questions or parts of questions are given in brackets [ ].

- Transactions should be recorded in the answer book.

- All calculations should be shown clearly.

- All working, including rough work, should be done on the same page as, and adjacent to the rest of the answer.

Section-A

Part – I (12 Marks)

Answer all questions.

Question 1. [6×2]

Answer briefly each of the following questions :

(i) Name the account which is prepared to find the profit and loss of a joint venture, if:

(a) One co-venture records all transactions.

(b) All co-ventures record their own transactions.

(ii) What will be the treatment of loan given to a partner by the firm at the time of its dissolution ?

(iii) Give the adjusting entry for interest on capital allowed to a partner, when the firm follows the fixed capital method.

(iv) State, with reason, whether securities premium reserve can be used to write off bad debts.

(v) Give any two differences between a Company s Balance Sheet and a Firm’s Balance Sheet.

(vi) State where will the non-cash transactions be recorded at the time of issue of shares, if all cash transactions are entered in the Cash Book.

Answer:

(i) (a) Joint Co-venture Account

Personal Accounts of other Co-ventures

(b) Memorandum Joint Venture Account

Joint Venture with…. (other Co-venture) Account

(ii) If there is a loan advanced to a partner, the same should be transferred to his capital account thereby reducing the amount of capital repayable to him.

(iii) Interest on Capital A/c Dr.

To Partner’s Current A/c

(Being the interest on capital allowed to partners)

Profit and Loss Appropriation A/c Dr.

To Interest on Capital A/c

(Being the interest on capital transferred to Profit and Loss Appropriation A/c)

(iv) Securities Premium Reserve cannot be used to write off bad debts.

Securities Premium Reserve can be write off for following purposes :

- in paying up unissued shares to be issued as fully paid bonus shares.

- in writing off preliminary expenses.

- for buy – back of shares Under Section 11 A.

- in writing off the expenses etc.

(v) Balance Sheet is prepared as per Schedule III of the Indian Companies Act, 2013. Whereas Balance Sheet is prepared as per Partnership Act, 1932. The details of items of Balance Sheet are to be given in the Notes to Accounts in Company’s Balance Sheet but there is no need to maintain Notes to Accounts in firm’s Balance Sheet.

(vi) Issue of Shares for Consideration other than Cash is shown in the Balance Sheet under the head ‘Share Capital’ and sub-head ‘Subscribed Capital’.

Part – II (48 Marks)

Answer any four questions.

Question 2. [12]

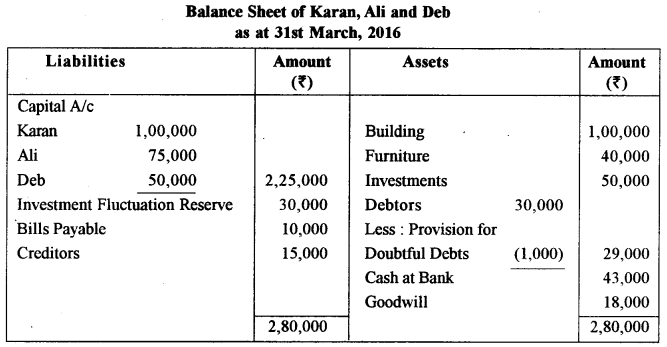

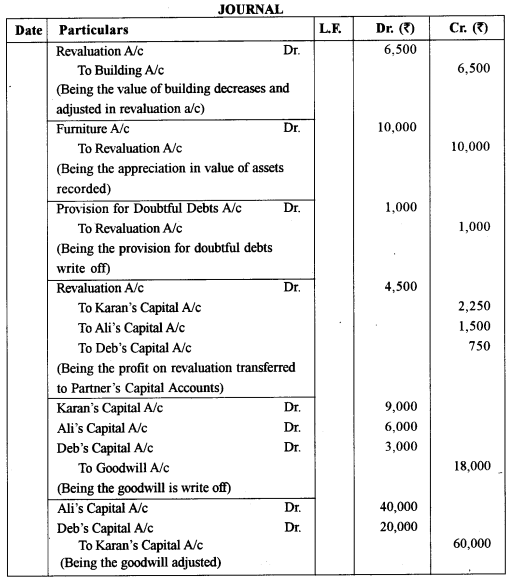

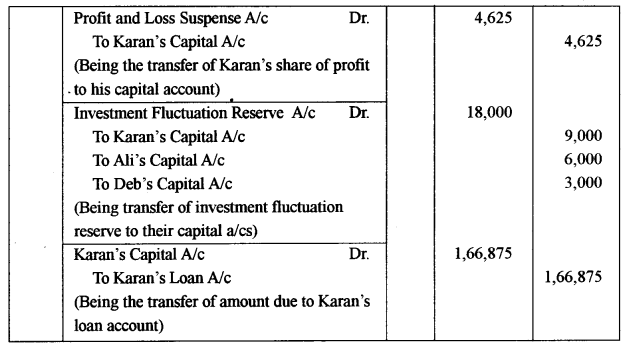

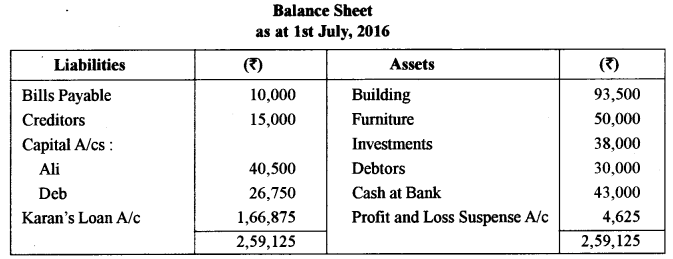

Karan, Ali and Deb are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. On 31st March, 2016, their Balance Sheet was as under :

Karan died on 1st July, 2016. An agreement was reached amongst Ali, Deb and Karan’s legal representatives that :

(a) Building be revalued at ₹ 93,500.

(b) Furniture be appreciated by ₹ 10,000.

(c) To write off the Provision for Doubtful Debts since all debtors were good. .

(d) Investments be valued ₹ 38,000.

(e) Goodwill of the firm be valued at ₹ 1,20,000.

(f) Karan’s share of profit to the date of his death, to be calculated on the basis of previous year’s profit which was ₹ 25,000.

(g) Interest on capital to be allowed on Karan’s capital @ 6% per annum.

(h) Amount payable to Karan’s legal representative to be transferred to his legal representative’s loan account.

You are required to :

(i) Pass Journal entries on the date of Karan’s death.

(ii) Prepare the Interim Balance Sheet of the reconstituted firm.

Answer:

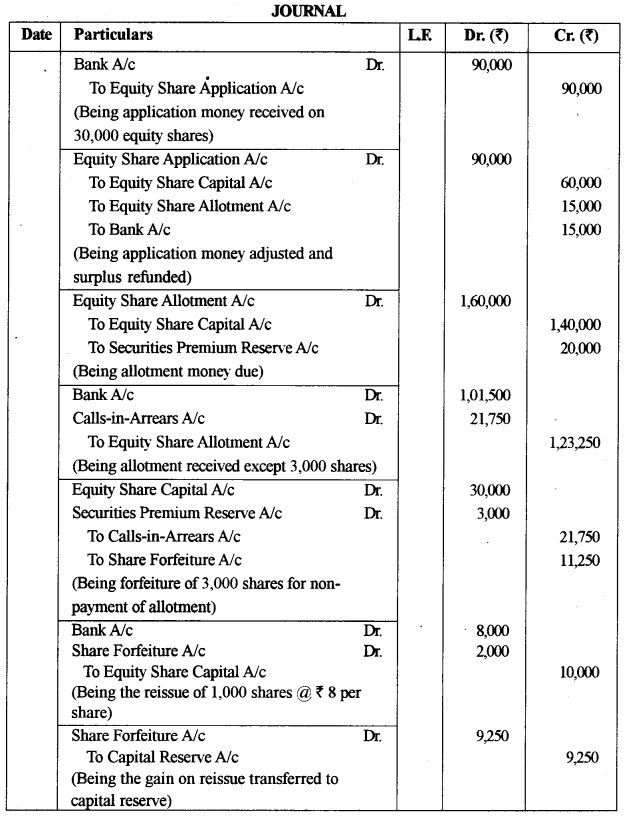

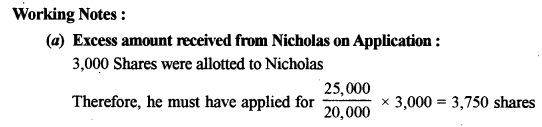

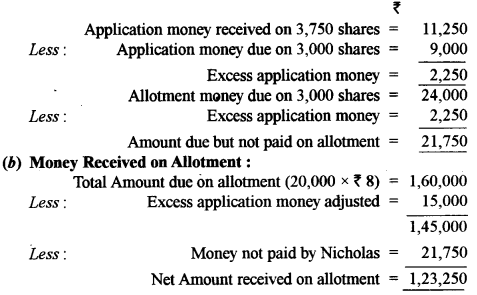

Question 3. [12]

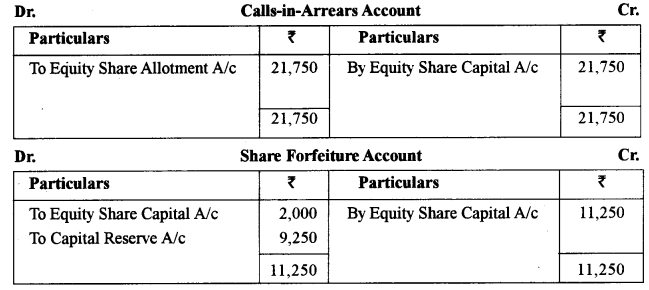

Cargo Ltd. invited applications for the issue of 20,000 Equity shares of ? 10 each at a premium of ? 1 per share, payable as follows :

On Application — ₹ 3

On Allotment — The balance (including premium ₹ 1)

Applications were received for 30,000 shares and pro-rata allotment was made to the remaining applicants after refunding application money to 5,000 share applicants.

Nicholas, who was allotted 3,000 shares, failed to pay the allotment money and his shares were forfeited.

Out of these forfeited shares, 1,000 shares were reissued as fully paid-up @ ? 8 per share.

You are required to :

(i) Pass Journal entries in the books of the company.

(ii) Prepare Calls-in-Arrears Account.

(iii) Prepare Share Forfeiture Account.

Answer:

Question 4.

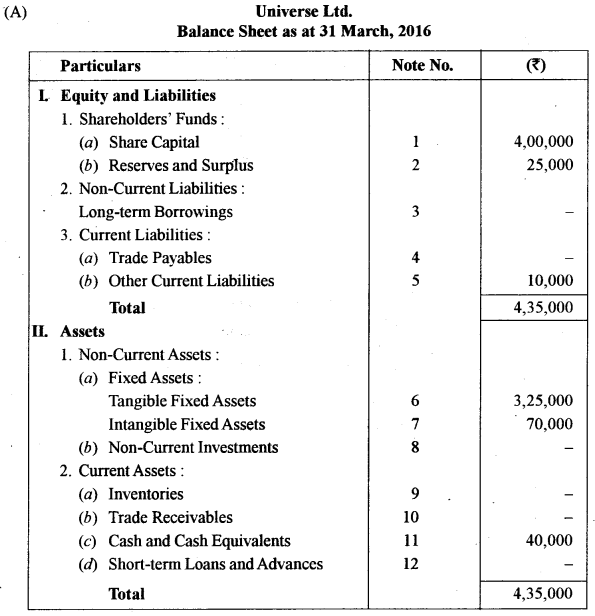

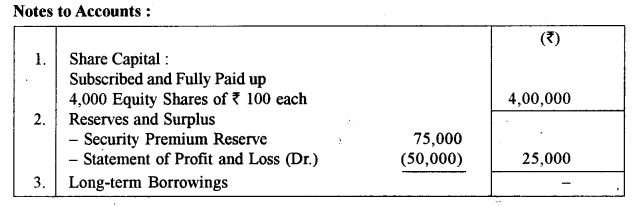

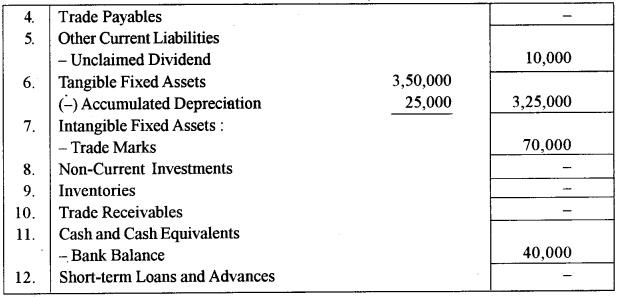

(A) Following balances have been extracted from the books of Universe Ltd. as at 31st March, 2016 :

Particulars

Equity Share Capital (Fully paid shares of ₹ 100 each) — ₹ 4,00,000

Unclaimed Dividend — ₹ 10,000

Bank Balance — ₹ 40,000

Security Premium Reserve — ₹ 75,000

Statement of Profit and Loss (Dr.) — ₹ 50,000

Tangible Fixed Assets (at cost) — ₹ 3,50,000

Accumulated Depreciation till date — ₹ 25,000

Trade Marks — ₹ 70,000

You are required to prepare as at 31st March, 2016 :

(i) The Balance Sheet of Universe Ltd. as per Schedule in of the Companies Act, 2013.

(ii) Notes of Accounts. . [8]

(B) Chrome Ltd. took over assets of ₹ 6,00,000 and liabilities of ₹ 40,000 of Polymer Ltd. at an . agreed value of ₹ 6,30,000. Chrome Ltd. issued 10% Debentures of ₹ 100 each at a discount of 10% to Polymer Ltd. in full satisfaction of the price. Chrome Ltd. writes off any capital losses incurred during a year, at end of that financial year.

You are required to pass the necessary Journal entries to record the above transactions in the books of Chrome Ltd. [4]

Answer:

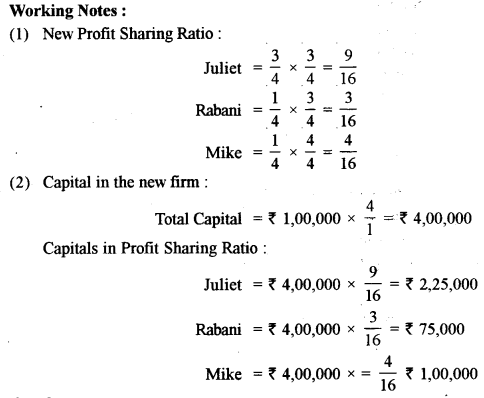

Question 5. [12]

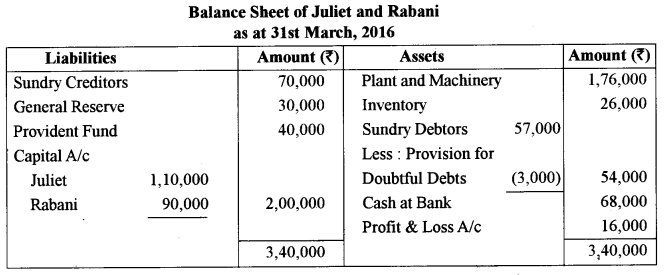

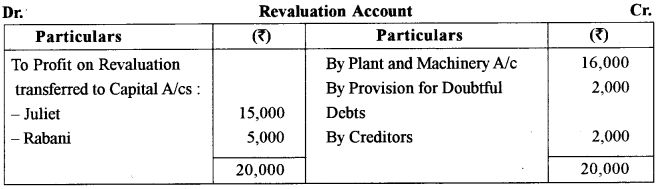

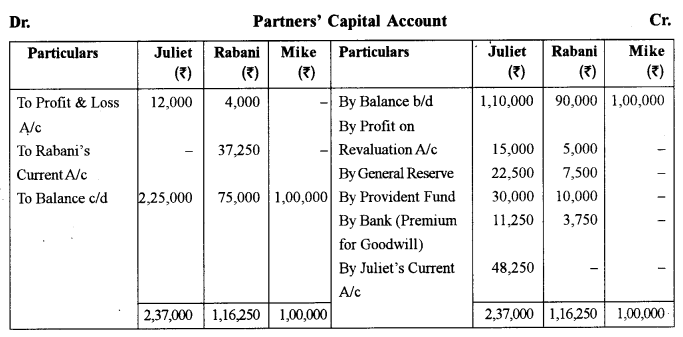

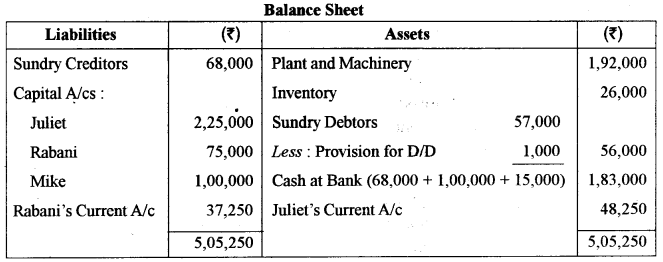

Juliet and Rabani are partners in a firm, sharing profits and losses in the ratio of 3 :1. On 31 st March, 2016, their Balance Sheet was as under:

Mike was taken as a partner for 1/4th share, with effect from 1st April, 2016, subject to the following adjustments :

(a) Plant and Machinery was found to be overvalued by ₹ 16,000. It was to be shown in the books at the correct value.

(b) Provision for Doubtful Debts, was to be reduced by ₹ 2,000.

(c) Creditors included an amount of ₹ 2,000 received as commission from Malini. The necessary adjustment was required to be made.

(d) Goodwill of the firm was valued at ₹ 60,000. Mike was to bring in cash, his share of goodwill along with his capital of ₹ 1,00,000.

(e) Capital Accounts of Juliet and Rabani were to be readjusted in the new profit sharing arrangement on the basis of Mike’s capital, any surplus to be adjusted through current account and any deficiency through cash.

You are required to prepare r

(i) Revaluation Account.

(ii) Partners’ Capital Accounts.

(iii) Balance Sheet of the reconstituted firm.

Answer:

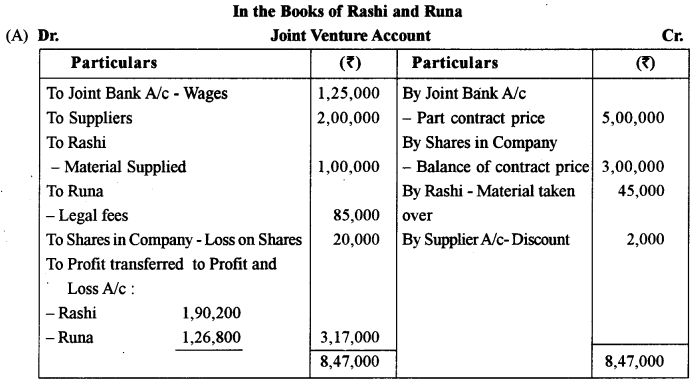

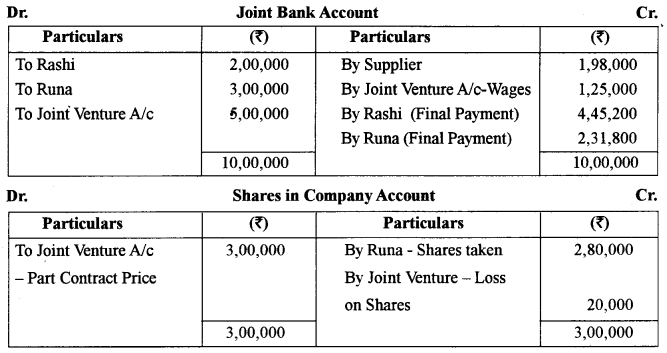

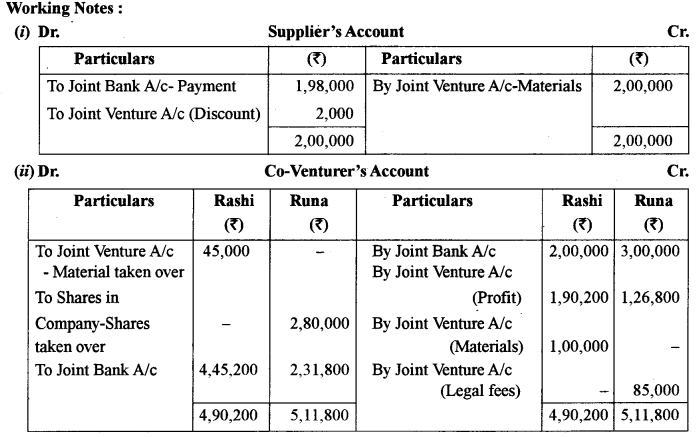

Question 6.

(A) Raslii and Runa jointly imdertake to complete the construction of an auditorium for Pascal Ltd. They agreed to share profits and losses in the ratio of 3 : 2.

The contract price was ₹ 8,00,000 of which ₹ 5,00,000 was to be payable to them in cash and the balance in fully paid shares of the company.

A joint bank account was opened in which Rashi contributed ₹ 2,00,000 while Runa contributed ₹ 3,00,000.

The following expenses were incurred to complete the contract :

Salaries and Wages — ₹ 1,25,000

Purchase of material from a supplier on credit — ₹ 2,00,000

Material supplied by Rashi — ₹ 1,00,000

Legal fees paid by Runa — ₹ 85,000

The contract price was duly received after the completion of the project and the accounts of the venture were closed after the supplier was paid ₹ 1,98,000 in lull and final settlement.

Runa took over the shares at ₹ 2,80,000.

Rashi took over the remaining material at ₹ 45,000.

You are required to prepare:

(i) Joint Venture Account.

(ii) Joint Bank Account.

(iii) Shares Account.

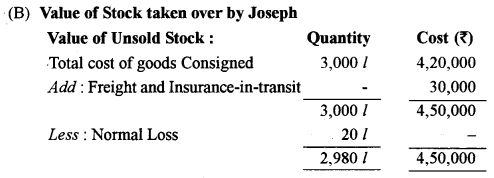

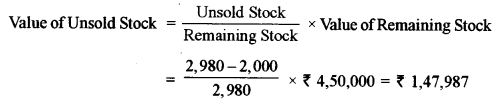

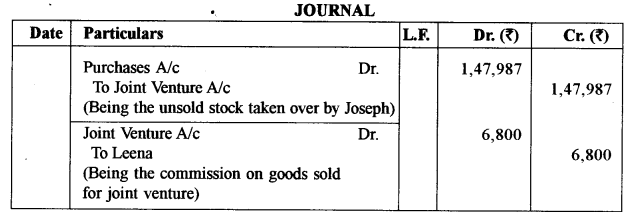

(B) Joseph and Leena entered into a Joint venture to sell edible oil. It was decided that Joseph would record all the transactions of the venture.

Joseph supplied 3,000 litres of edible oil costing ₹ 4,50,000 to be sold by Leena, incurring carriage and insurance-in-transit amounting to ₹ 30,000.

20 litres of oil was lost in transit due to leakage which was considered to be normal. Leena incurred ₹ 2,760 as clearing charges and ₹ 2,000 as godown rent. She was entitled to a commission of 2% on the sales made by her.

Leena was able to sell 2,000 litres of oil at ₹ 170 per litre.

The unsold stock was taken over by Joseph at the original cost plus proportionate non-recurring expenses.

You are required to :

(i) Calculate the value of stock taken over by Joseph.

(ii) Pass the relevant Journal entries in the books of Joseph for :

(a) The stock taken over by Joseph.

(b) Commission due to Leena. [4]

Answer:

Question 7.

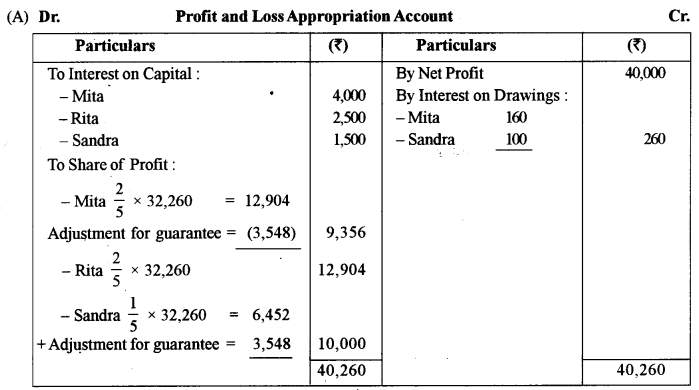

(A) Mita, Rita and Sandra were partners in a firm, sharing profits and losses in the ratio of 2 : 2 : 1. Mita had personally guaranteed that in any year Sandra’s share of profit, after allowing interest on capital to all the partners @ 5% per annum and charging interest on drawings @ 4% per annum, would not be less than ₹ 10,000.

The capitals of the partners on 1st April, 2015 were :

Mita ₹ 80,000, Rita ₹ 50,000 and Sandra ₹ 30,000.

The net profit for the year ended 31st March, 2016, before allowing or charging any interest amounted to ₹ 40,000.

Mita had withdrawn ₹ 4,000 on 1st April, 2015, while Sandra withdrew ₹ 5,000 during the year.

You are required to prepare the Profit and Loss Appropriation Account for the year 2015-16. [8]

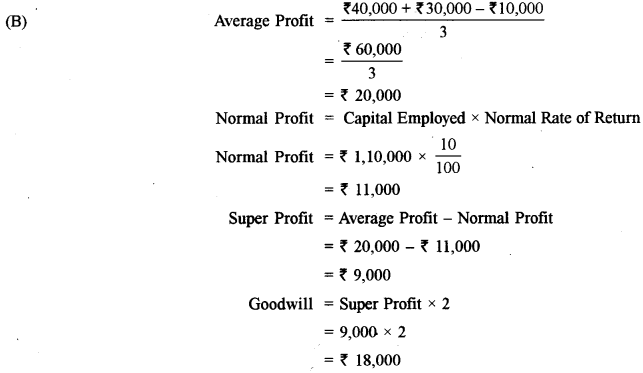

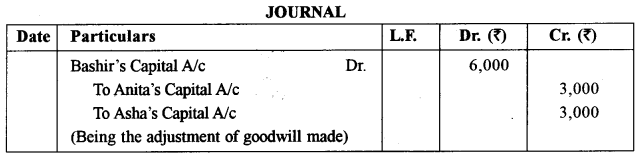

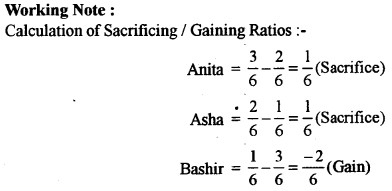

(B) Anita, Asha and Bashir are partners sharing profits and losses in the ratio of 3 : 2 : 1 respectively. From 1st April 2016, they decided to change their profit sharing ratio to 2 : 1: 3. Their partnership deed provides that in the event of any change in the profit changing ratio, the goodwill of the firm should be valued at two years’ purchase of the average super profits for the past three years.

The actual profits and losses for the past three years were :

2015-16 Profit ₹ 40,000

2014-15 Profit ₹ 30,000

2013-14 Loss ₹ 10,000

The average capital employed in the business was ₹ 1,10,000; the rate of interest expected from capital invested was 10%.

You are required to:

(i) Calculate the value of goodwill at the time of change in profit sharing ratio. (Show the workings clearly with the formulae.)

(ii) Pass the Journal entry to record the change. [4]

Answer:

Question 8.

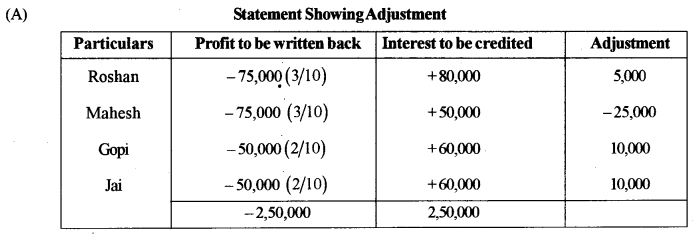

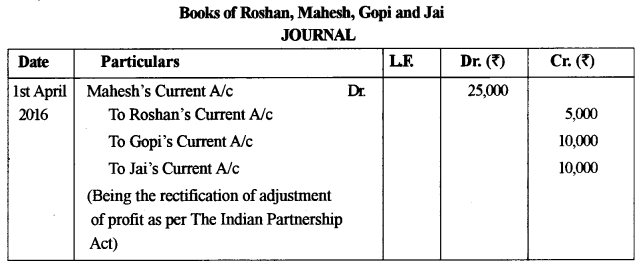

(A) Roshan, Mahesh, Gopi and Jai are partners sharing profits and losses in the ratio of 3 : 3 : 2 : 2. The balances of capital accounts on 1st April, 2015 were : Roshan ₹ 8,00,000, Mahesh ₹ 5,00,000, Gopi ₹ 6,00,000 and Jai ₹ 6,00,000.

After the accounts for the year ended 31st March, 2016 were prepared, it was discovered that interest on capital @ 10% per annum as provided in the partnership deed had not been credited to the partners’ capital accounts before the distribution of profits.

You are required to rectify the error by passing a single adjusting Journal entry. [4]

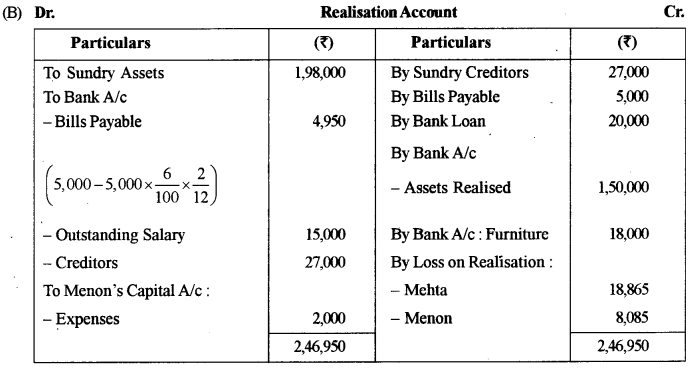

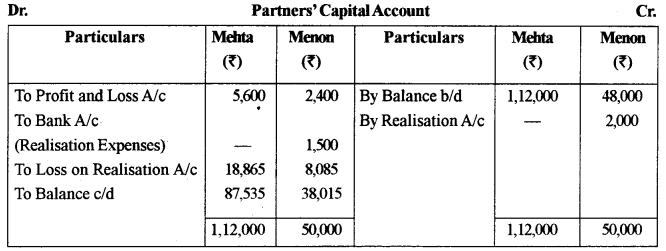

(B) Mehta and Menon were partners in a firm, sharing profits and losses in the ratio of 7 : 3.

They decided to dissolve their partnership firm on 31st March, 2016. On that date, their books showed the following ledger account balances :

Sundry Creditors ₹ 27,000

Profit and Loss A/c (Dr.) ₹ 8,000

Cash in Hand ₹ 6,000

Bank Loan ₹20,000

Bills Payable ₹ 5,000

Sundry Assets ₹ 1,98,000

Capital A/c

Mehta ₹ 1,12,000

Menon ₹ 48,000

Additional information :

(a) Bills Payable falling due on 31st May, 2016 were retired on the date of dissolution of the firm, at a rebate of 6% per annum.

(b) The bankers accepted the furniture (included in sundry assets) having a book value of ? 18,000 in full settlement of the loan given by them.

(c) Remaining assets were sold for ₹ 1,50,000.

(d) Liability on account of outstanding salary not recorded in the books, amounting to ₹ 15,000 was met.

(e) Menon agreed to take over the responsibility of completing the dissolution work and to bear all expenses of realization at an agreed remuneration of ₹ 2,000. The actual realization expenses were ₹ 1,500 which were paid by the firm on behalf of Menon.

You are required to prepare :

(i) Realization Account.

(ii) Partners’ Capital Accounts. [8]

Answer:

Section – B

(20 Marks)

Answer any two questions

Question 9.

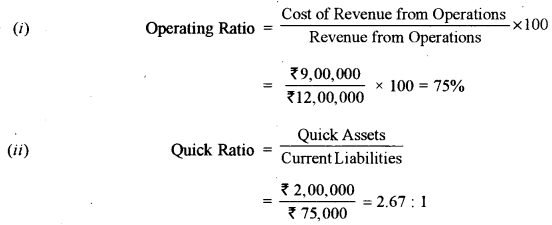

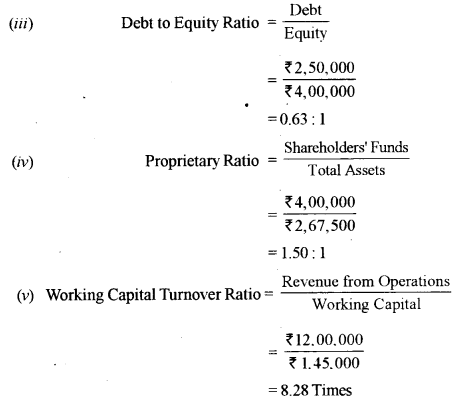

From the information given below, calculate (up to two decimal places):

(i) Operating Ratio.

(ii) Quick Ratio.

(iii) Debt to Equity Ratio.

(iv) Proprietary Ratio.

(v) Working Capital Turnover Ratio.

Particulars

Net revenue from operations — ₹ 12,00,000

Cost of revenue from operation — ₹ 9,00,000

Operating expenses — ₹ 15,000

Inventory — ₹ 20,000

Other Current Assets — ₹ 2,00,000

Current Liabilities — ₹ 75,000

Paid up Share Capital — ₹ 4,00,000

Statement of Profit and Loss (Dr.) — ₹ 47,500

Total Debt — ₹ 2,50,000

Answer:

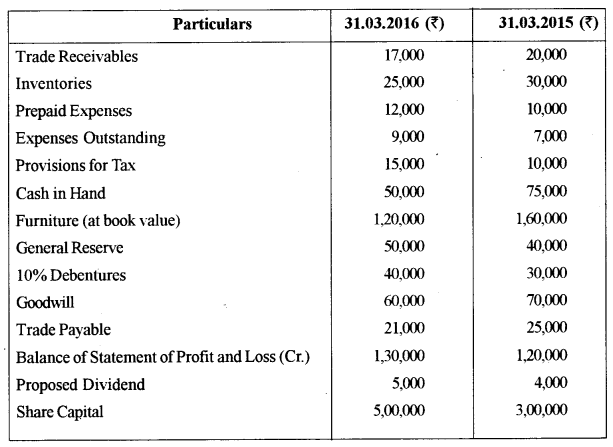

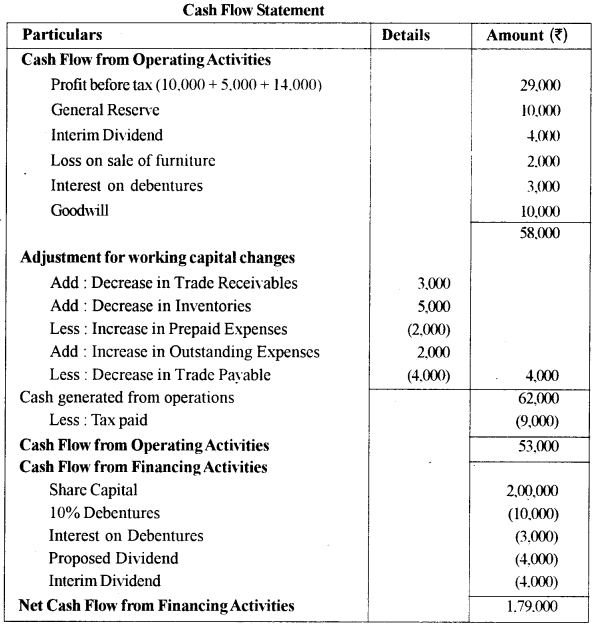

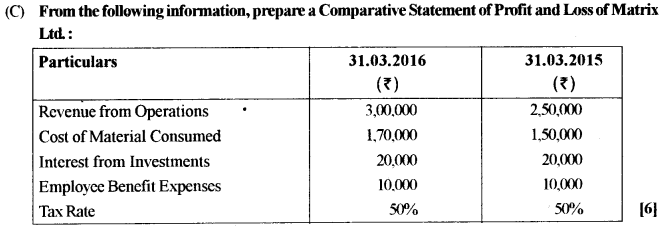

Question 10. [10]

From the following information of Purity Ltd. calculate:

(i) Cash from Operating Activities

(ii) Cash from Financing Activities

Additional information:

During the year 2015-16:

(a) A piece of furniture costing ₹ 30.000 (accumulated depreciation ₹ 5,000) was sold for ₹ 25,000.

(b) Tax of ₹ 9,000 w as paid.

(c) Interim Dividend of ₹ 4,000 was paid.

(d) The company paid ₹ 3,000 as interest on debentures.

Answer:

Question 11.

(A) What is meant by the term Cash Equivalents as per Accounting Standard 5 ? [2]

(B) The Current Ratio of a company is 2 : 1. State whether the Current Ratio will improve, decline or will not change in the following cases : [2]

(i) Bill Receivable of ₹ 2,000 endorsed to a creditor is dishonoured.

(ii) ₹ 8,000 cash collected from Debtors of ₹ 8,500 in lull and final settlement.

Answer:

(A) Cash and Cash Equivalents are short-term, highly liquid investments which is easily converted into cash. It includes treasury bills, commercial papers, money market funds etc.

(B) (i) It will increase the amount of debtors but reduces the amount of bills receivable. So, current assets will remain same. Hence, there will be no change in the current ratio.

(ii) Cash collected from debtors will increase the bank/cash balance but decrease the amount of debtors. Hence, total current assets remain unchanged. Therefore, there will be no . change in current ratio.